The markets have soared in the past two weeks with word of tariff relief. It was accompanied by reduced concern about a potential recession and greater confidence in US corporate earnings engines. Adding to this optimism is that corporate administrative costs in dealing with regulatory red tape and fears of SEC fines have been relegated to the past – at least for now. Reduced corporate costs in money and time equal more profitability. However, there may ultimately be another side to requiring less corporate transparency. Earnings can be fabricated, and accounting tricks can come to the forefront following an after-the-fact discovery of fraud. Think in terms of WeWork, Valeant, Enron and Lehman Brothers.

All 5,200+ stocks US and Canadian stocks, 16 sector groups, 200+ industries, and 700+ ETFs have been updated: Two-week free trial: www.ValuEngine.com

With this in mind, a relatively new index-driven ETF launched by First Trust last October has captured our interest. The First Trust New Constructs Core Earnings Leaders ETF, with ticker symbol FTCE, uses artificial intelligence (AI) to target a company’s “true earnings” by measuring accounting transparency. The underlying index is The Bloomberg New Constructs 500 Index. Its Bloomberg ticker is B500NCT. The index tracks the performance of companies in Bloomberg US Large Cap Index with their weight tilted towards companies with high Earnings Capture using data from New Constructs. The Earnings Capture metric determines the difference between reported and core earnings by removing unusual gains and losses found in certain sections of company filings.

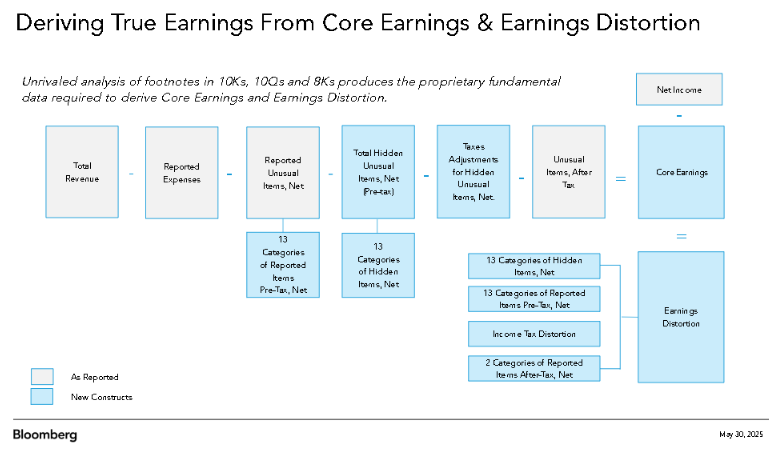

A quote from the Bloomberg Indices’ specs page on this index spells out how this index and its associated ETF differ from standard quality “smart beta” ETFs such as QUAL from iShares. “While the Bloomberg Index team has access to vast sets of differentiated data and unique insights, the partnership with New Constructs leverages an AI-based parsing process and machine learning technology to target a company’s Core Earnings by going beyond as-reported fundamentals and into the footnotes – which research shows the market is missing. This process is known as Earnings Capture as demonstrated in the following diagram from Bloomberg Research.”

Current ValuEngine reports on all covered stocks and ETFS can be viewed HERE

New Constructs leverages its decades of experience in technology-driven data collection and analysis to provide investors with empirically proven superior, unbiased research to generate novel alpha. The Bloomberg page then goes on to depict how core earnings of a company is captured by showing New Constructs’ adjustments for hidden items buried in footnotes such as non-operating expenses, cash taxes on core earnings, unreported employee stock option expense, and more. In most cases, the distortions between reported earnings and core earnings can be zero or minimal. The stocks of the companies where the discrepancies are non-trivial are rejected from consideration for the index. The removal of the stocks of these companies provides the source of the alpha demonstrated by the index so far.

FTCE has been able to replicate the alpha of its index year-to-date and for the most recent 3- and 6-month periods. FTCE did underperform its benchmark in the most recent 1-month period. These numbers are even after allowing for its non-trivial expense ratio of 0.60%, This is not always a given for new ETFs. Another plus as a potential core investment is that the underlying index tracks the S&P 500 reasonably closely while posting slightly lower volatility and less overvalued price-to-earnings, price-to- book and price-to-cash-flow ratios.

In about nine months of trading, these are the returns and relevant ratios for FTCE in comparison with the SPDR S&P 500 ETF (SPY):

| Data as of 5/28/2025 | |||||||

| 1-mo returns | 3-mo returns | 6-mo Returns | YTD returns | P/E | P/S | P/BV | |

| FTCE | 5.61% | -4.03% | -1.01% | 4.02% | 20.87 | 1.89 | 3.79 |

| SPY | 6.02% | -7.50% | -0.52% | 0.80% | 25.83 | 3.026 | 4.99 |

Current ValuEngine reports on all covered stocks and ETFS can be viewed HERE

While FTCE is conceptually appealing with two strong brands, Bloomberg and First Trust, behind the conceptual creation of New Constructs investors must consider a number of risk factors beyond those endemic to US equity market investing. With assets under management around the $50 million level and less than a one-year track record, FTCE will not qualify for many brokerage platforms. This is important for several reasons. It can widen the bid-ask spread for small trades. Since the underlying stocks are liquid, call a First Trust representative for trades of 1,000 shares or more where the ETF’s market-makers could be helpful. Another thing customers of brokers with platforms not supporting FTCE can do is to call their sales agent to request purchase. Some platforms allow that. That said, platforms cite risk management as a reason for having those rules. So, investors should do extra due diligence. Some may wish to put FTCE on a personal watch list to monitor its progress. Also, even a strong AI footnote reader/interpreter cannot detect all potential landmines that companies may encounter. Another risk for all small ETFs is that the sponsor may choose to close them if they do not garner a sufficient total asset level to clear the aforementioned hurdles.

ETF closings are not as daunting as that sounds. An ETF’s “collateral” comprises the assets it holds. Therefore, investors will receive the net asset value of the assets held which are unaffected by the fund’s closing. However, receiving that cash and needing to reinvest it is an event some investors choose not to risk. Finally, the reason you read that past performance does not guarantee future results is that all investment strategies are time-period dependent, subject to market cyclicality and unexpected corrections and crashes. This is as true for FTCE as it is for any investment product and perhaps even more true for nascent strategies and ETFs using them. We also encourage our readers to be aware of the risks involved that we couldn’t identify and the individual due diligence that should be performed before investing.

Financial Advisory Services based on ValuEngine’s research models: www.ValuEngineCapital.com

The bottom line is that FTCE appears to have the potential to avoid the “hidden risks” of inflated earnings in SEC Filings and capture better risk-adjusted returns than S&P 500 ETFs even after its larger expense ratio is deducted in the return calculation.

We featured this ETF because we found intriguing the underlying strategy of allowing AI to detect and remove companies that reported earnings that might be inflated and/or non-replicable. In a lax regulatory environment relative to prior Administrations, this “smart beta” factor may have great appeal to many US core equity investors.

_____________________________________________________________________

By Herbert Blank

Senior Quantitative Analyst, ValuEngine Inc ( www.ValuEngine.com )

support@ValuEngine.com

(321) 325-0519

All the over 4,200 stocks, 16 sector groups, over 250 industries, and 600 ETFs have been updated on www.ValuEngine.com

Financial Advisory Services based on ValuEngine research available through ValuEngine Capital Management, LLC

Free Two-Week Trial to all 5,000 plus equities and ETFs covered by ValuEngine HERE

Subscribers log in HERE